As global economies navigate shifting monetary policies and fluctuating consumer prices, investors continually evaluate the relative merits of precious metals versus tangible holdings. Examining the long-term trends in the gold market and comparing them with other assets can help determine which investments deliver superior protection against persistent inflation. This analysis delves into historical data, underlying mechanisms, and practical considerations for those seeking to hedge their portfolios.

Historical Performance of Gold and Tangible Holdings

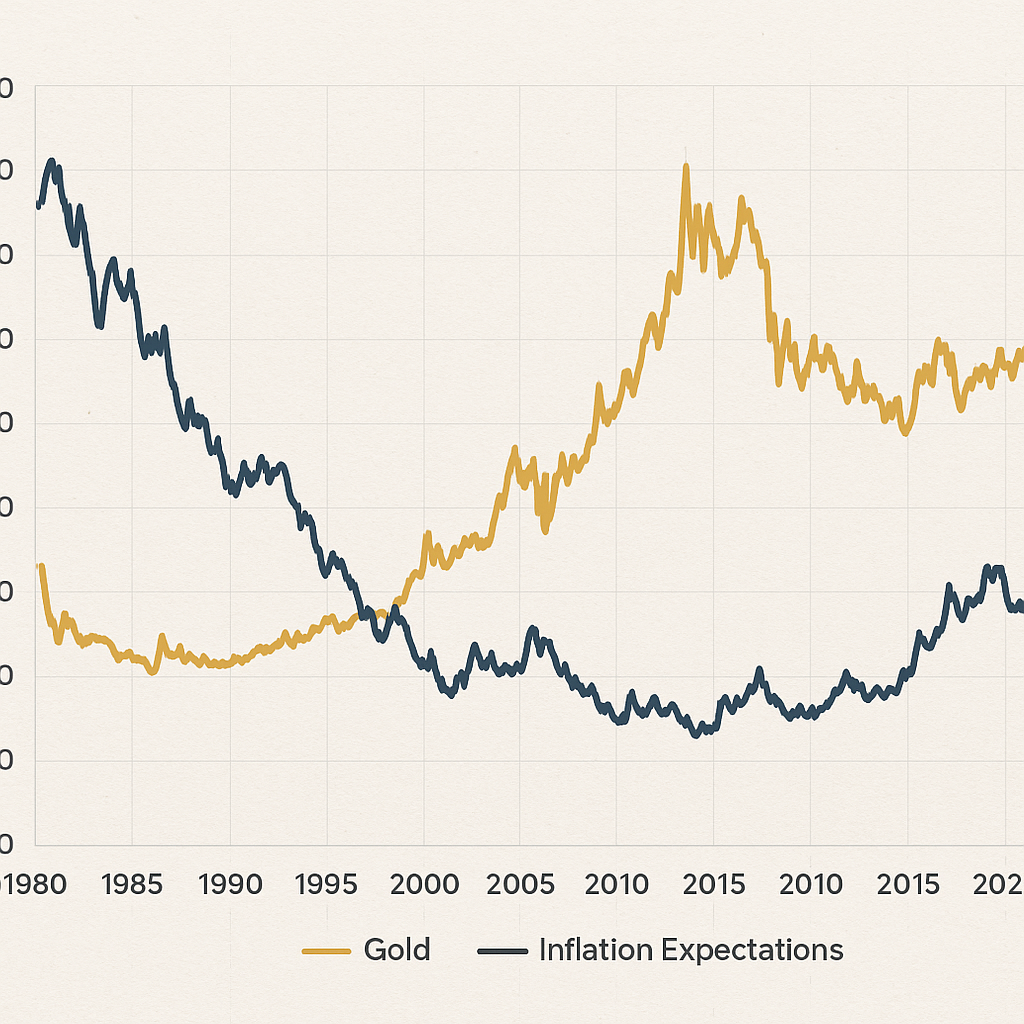

The journey of gold as a store of value spans millennia, but modern price data offers the clearest insight into its behavior through various economic cycles. From the collapse of the Bretton Woods system in 1971 to the 2008 global financial crisis and beyond, gold has often served as a safe haven. In contrast, other real assets such as real-estate, commodities like oil, and agricultural land exhibit distinct performance patterns.

Gold Price Trends Over Decades

- 1970s Surge: After the US decoupled the dollar from gold, the precious metal’s price skyrocketed from under $40 per ounce in 1971 to nearly $850 by 1980.

- 1980s–1990s Consolidation: Prices retreated and stabilized between $300–$400 through much of this period, as inflation rates moderated.

- Early 2000s Bull Run: Central banks’ aggressive liquidity injections and a weakening dollar propelled gold past $1,000 per ounce in 2008.

- Post-Financial Crisis: Gold peaked above $1,900 in 2011, then oscillated between $1,050–$1,500 until renewed inflation fears after 2020 drove prices back above $2,000.

Tangible Asset Growth and Cyclicality

While gold is often lauded for its relatively low correlation with equities, real-estate and agricultural land experience their own cycles. During periods of economic expansion, property values and farm commodity prices can outpace inflation, driven by structural demand. However, downturns often trigger volatility.

- Real-Estate: Driven by interest rates and credit availability, residential and commercial property values have grown at 3–5% above inflation on average in many developed markets over 30 years.

- Agricultural Land: Returns have tracked global food demand and weather patterns, with cumulative gains of 4–6% annually in prime regions.

- Energy Commodities: Prices for oil and natural gas have displayed high volatility due to geopolitical shocks, leading to short-term spikes but inconsistent long-term protection.

Mechanisms of Inflation Protection

Why does gold often shine brighter during inflationary regimes? The answer lies in its inherent characteristics compared to other real assets:

Finite Supply Versus Reproducibility

Gold’s scarcity is enforced by geological constraints. Unlike fiat currencies that can be printed, or farmland that can be expanded, gold’s above-ground stock grows by less than 2% annually through mining. This limited supply contrasts sharply with expanding money bases, preserving its purchasing power over time. In contrast, a house can be built and a crop can be planted, diluting scarcity.

Intrinsic Market Demand and Sentiment

Investor psychology plays a role: when confidence in monetary authorities diminishes, demand for a non-sovereign store of value spikes. Gold is also used in industry and jewelry, sustaining a baseline level of consumption. Meanwhile, property markets depend on credit conditions; if central banks hike rates to combat inflation, real-estate borrowing costs rise, potentially curbing price growth.

Income Generation Versus Pure Store of Value

One key distinction is that some real assets produce income streams—rent from property, dividends from infrastructure projects, or yields from agricultural leases. These cash flows can rise with inflation, offering a dynamic hedge. Gold, by contrast, provides no yield. Its appeal stems solely from capital gains and diversification benefits, making it a non-income-generating but stable hedge.

Investment Considerations and Market Outlook

When allocating between gold and other tangible holdings, investors must weigh several factors beyond historical returns. Identifying optimal portfolio mixes requires attention to diversification, cost structures, liquidity, and regulatory implications.

Liquidity and Transaction Costs

Gold is traded globally on exchanges like COMEX and LBMA, offering high liquidity and tight bid-ask spreads. Physical delivery, though, incurs storage and insurance fees. ETFs have bridged the gap, providing paper-gold exposure at low expense ratios. Conversely, real estate suffers from high transaction costs (agent commissions, taxes, legal fees) and long holding periods. Agricultural land is less liquid still, often requiring specialized brokers and due diligence.

Risk Management and Volatility Profiles

Historically, gold has exhibited lower annualized volatility than many commodity markets but higher volatility than high-grade government bonds. Real-estate and infrastructure investments exhibit moderate volatility, but they are subject to leverage cycles and local market risk. Allocations must reflect an investor’s risk tolerance:

- Conservative Portfolios: May favor 5–10% gold as an insurance policy against systemic shocks, with a higher weight in government bonds and income-generating real assets.

- Balanced Portfolios: Could allocate 10–15% to gold, 25–35% to global property funds, and the remainder in equities and bonds.

- Aggressive Portfolios: Might tilt more heavily toward commodities and specialized real-estate sectors, with a modest gold position for shock protection.

Regulatory and Tax Implications

Each jurisdiction treats gold and property differently for tax purposes. Capital gains on gold held longer than a year may benefit from lower rates, while rental income and property appreciation often face both income and wealth taxes. Understanding these regulatory nuances is crucial to optimizing after-tax returns.

Future Outlook and Strategic Balance

Looking forward, central banks remain dominant players in the gold market, both as custodians and buyers. Their policies influence global liquidity, which in turn impacts gold prices. On the real-estate front, demographic shifts and urbanization will continue to drive demand, but developers face rising input costs and environmental regulations. Agricultural land yields may be pressured by climate change, even as food security concerns heighten.

- Gold: Likely to maintain its role as a hedge, especially if central bank balance sheets expand further.

- Real-Estate: Expected to deliver consistent income growth but with local market disparities.

- Agriculture: Returns hinge on technological adoption and water resource management.

Ultimately, combining gold’s proven inflation hedge with income-producing real assets can provide a balanced approach. Investors seeking maximum growth might overweight cyclical commodities, while those prioritizing stability may emphasize gold and high-quality property. By understanding the unique benefits and constraints of each investment vehicle, portfolios can be structured to navigate future inflationary and deflationary waves with resilience.