The intricate dance between global oil markets and the world gold price reveals a tapestry of economic forces, geopolitical tensions, and investor psychology. As two of the most traded commodities worldwide, oil and gold each respond to supply, demand, monetary policy, and risk sentiment. Yet, their interplay often provides deeper insights into market expectations and portfolio strategies.

Historical Interaction of Oil and Gold Markets

The relationship between oil and gold dates back decades, tracing its roots to the post–Bretton Woods era and the 1970s energy crises. As major producers and consumers adjusted to price shocks, both commodities became key barometers for global economic health. Over time, researchers observed periods of strong correlation when oil and gold moved in tandem, as well as intervals when their prices diverged sharply.

- 1970s Oil Shocks: Soaring crude prices driven by geopolitical conflict led to rampant inflation. Investors turned to gold as an inflation hedge.

- 1980s–1990s Stability: Lower oil volatility and stable monetary policy reduced gold’s appeal, weakening the correlation.

- 2000s Commodity Boom: Rapid industrialization in emerging markets pushed oil prices upward, rekindling investor interest in gold amid rising inflation fears.

Throughout these eras, shifts in global currency values—especially the US dollar—played a central role. Since oil trades predominantly in dollars, a weaker greenback often translates into higher oil prices and boosts gold’s allure as an alternative store of value.

Economic Drivers and Correlation Dynamics

Several fundamental economic factors underpin the oil-gold connection. Understanding these drivers can help market participants anticipate turning points and craft effective hedging strategies.

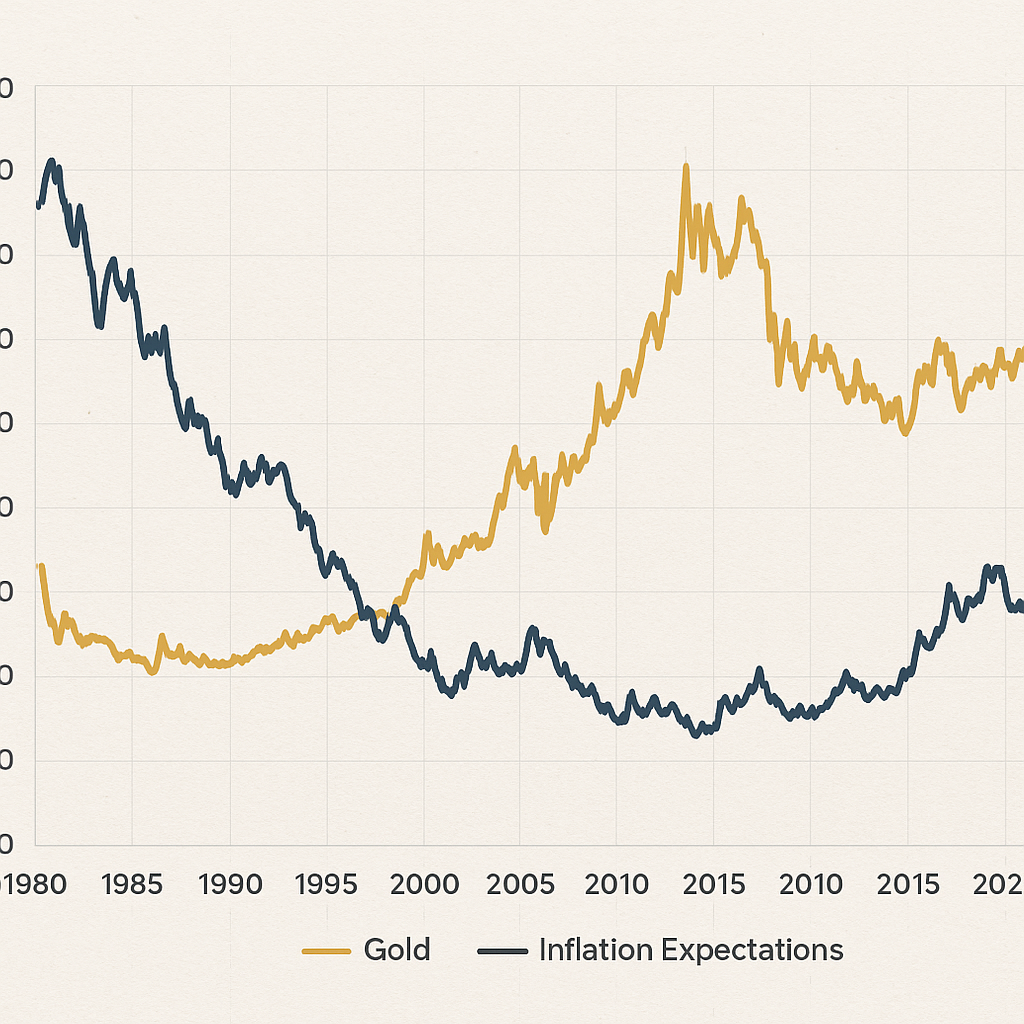

Inflation and Monetary Policy

- Inflation Expectations: Rising oil costs feed into broader consumer prices, prompting central banks to consider tightening. Anticipation of rate hikes can dampen gold’s appeal if real yields climb, yet stubborn inflation often propels investors back toward the metal.

- Interest Rate Divergence: When US rates outpace global peers, the dollar strengthens, capping oil gains. Conversely, dovish policies erode real yields and support both commodities as investors seek protection from currency debasement.

Supply–Demand Fundamentals

- Oil Production Shocks: Natural disasters, OPEC decisions, or sanctions can curtail output, spiking crude prices. This supply squeeze heightens economic uncertainty, fueling demand for gold.

- Gold Mine Output: Production costs, mining disruptions, and exploration success affect gold’s supply. Limited upside in supply during demand surges can accentuate price co-movements with oil.

While correlation metrics fluctuate, academic studies often find a modest positive link—especially during periods of rising volatility. In times of elevated market stress, both oil and gold frequently rally together, reflecting broad-based risk aversion and asset repricing.

Geopolitical Influences and Crisis Periods

Geopolitical tensions offer some of the clearest examples of oil and gold moving in concert. Fear-driven buying tends to uplift both markets, although the intensity and duration of these moves can vary.

Middle East Conflicts

- Supply Disruption Fears: Hostilities in key oil-producing regions trigger crude price spikes. In parallel, investors flock to gold as a safe haven.

- Regulatory Responses: Sanctions on major exporters constrain oil flows, reinforcing the metal’s haven status during geopolitical stand-offs.

Global Financial Turmoil

- Credit Crises: Financial market collapses often depress commodity demand, leading to initial sell-offs in oil. Gold, however, tends to stabilize or advance as liquidity crises heighten systemic risk concerns.

- Pandemic Shocks: The COVID-19 outbreak saw an unprecedented convergence: oil prices briefly turned negative in 2020 amid storage shortages, while gold surged on fears of economic collapse and ultra-loose monetary policy.

In each scenario, investors gauge the balance between growth prospects and monetary easing. If economic damage appears severe, gold’s protective premium can outweigh oil’s rebound potential.

Implications for Investors and Future Outlook

Portfolio managers and private investors alike monitor the oil-gold nexus to inform investment allocation decisions. Key strategies often include:

- Hedging Energy Exposure: Incorporating gold futures or ETFs can mitigate downside risk if energy-driven inflation accelerates.

- Currency Diversification: Hedging dollar exposure through gold may offset adverse moves when central banks pursue quantitative easing.

- Timing Commodity Swaps: Tactical shifts between oil equities and gold mining stocks capitalize on shifts in relative momentum and risk sentiment.

Looking ahead, several trends may reshape the oil-gold interplay:

- Energy Transition: The global shift toward renewable sources could dampen long-term oil demand. Lower structural demand for crude may reduce its inflationary impact, potentially weakening its link with gold.

- Digital Gold and Crypto: The rise of cryptocurrencies as alternative stores of value introduces fresh competition for gold’s safe-haven status, though oil’s role remains anchored in physical energy consumption.

- Monetary Policy Divergence: If developed economies return to tightening while emerging markets maintain looser stances, the resulting capital flows could produce asymmetric effects on oil and gold.

In this evolving landscape, understanding the nuanced relationship between two cornerstone risk assets—oil and gold—remains essential. Their historical patterns offer valuable lessons, yet adaptability to changing economic and geopolitical conditions will define successful strategies in the years to come.