The correlation between gold prices and global debt levels has fascinated investors, economists, and policymakers for decades. As national budgets bloat and sovereign borrowing accelerates, the yellow metal often responds in tandem, reflecting shifts in market sentiment and macroeconomic pressures. This article explores the multifaceted relationship between rising debt burdens and the trajectory of world gold price, offering insights into historical patterns, underlying drivers, real-world case studies, and future projections.

Historical Context of Gold and Debt Accumulation

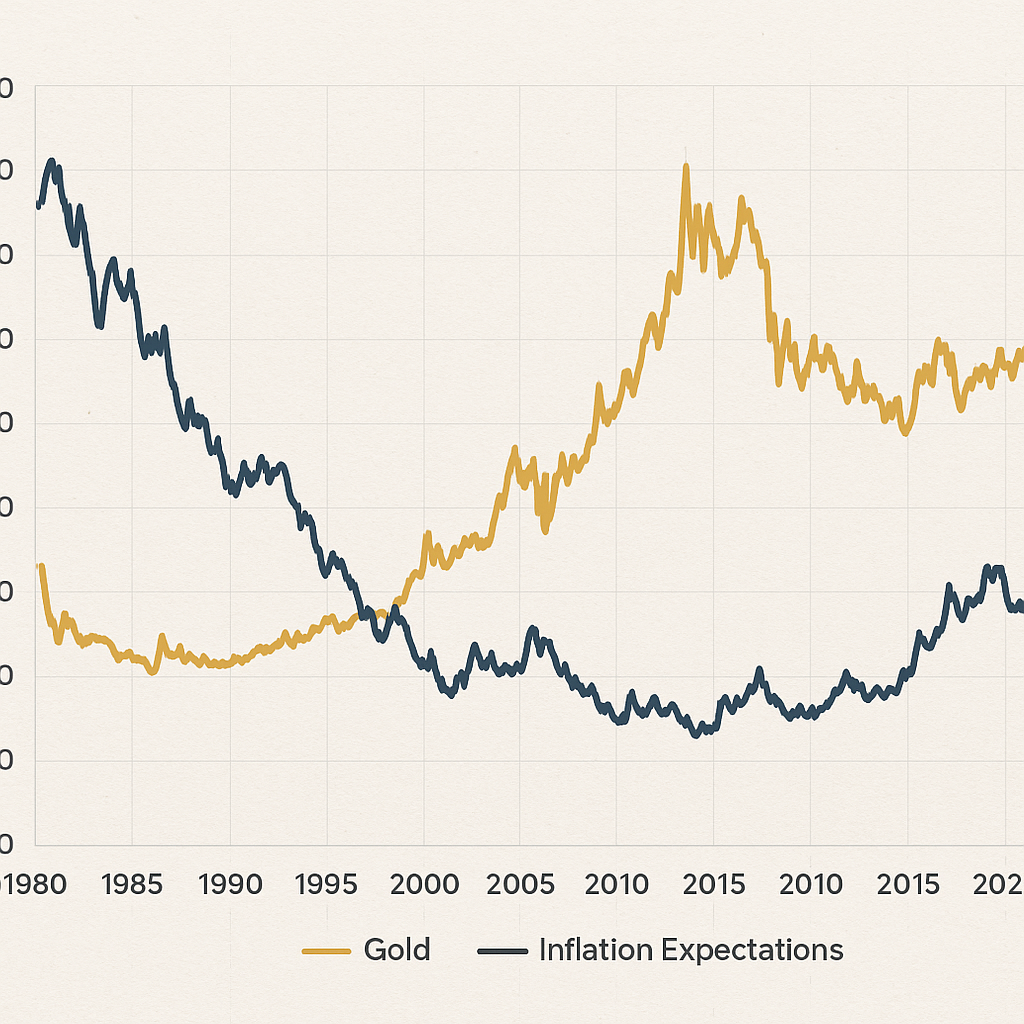

Over the last century, major economic upheavals—World War II, the collapse of the Bretton Woods system, multiple oil shocks, and the 2008 Global Financial Crisis—have driven both sovereign debt expansion and gold market volatility. In the aftermath of fiscal emergencies, many countries turned to borrowing as a short-term remedy. Meanwhile, investors sought the security of a physical asset unlinked to any single currency or central bank policy.

Pre-1971 Monetary Regime

Under the gold-backed dollar standard, central banks held gold reserves to back their currency issuance. Debt-to-GDP ratios remained relatively modest, as monetary expansion was constrained by reserve requirements. Nonetheless, rising defense expenditures and post-war reconstruction started pushing sovereign borrowings upward, setting the stage for future shifts.

Post-1971 Floating Exchange Rates

The end of the gold convertibility era unleashed a new dynamic. Fiat currencies allowed governments to increase debt issuance without immediate reserve constraints. Simultaneously, gold prices began to float freely, surging during periods of heightened inflation expectations. By the late 1970s, gold had reached record highs, driven by expansive fiscal and monetary policies worldwide.

Drivers of the Gold-Debt Relationship

Several mechanisms explain why gold prices often rise alongside growing sovereign indebtedness. Understanding these factors is crucial for both strategic asset allocation and policy evaluation.

- Inflation Expectations: As governments borrow extensively, the risk of monetizing debt increases. Investors anticipate higher price levels, boosting gold’s appeal as a hedge.

- Liquidity Crunch: During debt-fueled downturns, central banks inject liquidity to stabilize markets. Excess money supply can erode fiat currency values, pushing up gold valuations.

- Fiscal Imbalance: Large budget deficits often signal unsustainable fiscal paths. Gold acts as a safe store of value when confidence in government finances wanes.

- Currency Depreciation: High debt ratios can weaken a nation’s currency. As exchange rates suffer, dollar-priced gold becomes more expensive domestically and globally.

- Risk Aversion: In times of sovereign default fears, investors rotate from equities and bonds into gold, seeking capital preservation.

Behavioral Finance Perspectives

From a psychological standpoint, gold trading reflects collective sentiment toward government solvency. Herding behavior amplifies price swings when fiscal concerns dominate headlines. Speculative flows can exacerbate short-term volatility, though long-term trends often correlate with macroeconomic fundamentals.

Case Studies of Debt Crises and Gold Price Reactions

Examining specific episodes helps illustrate how debt dynamics influence gold markets in real time.

1980s Latin American Debt Debacle

Several Latin American nations faced ballooning external debts and skyrocketing interest rates in the early 1980s. During this period:

- Gold prices soared from around $200 per ounce in 1978 to over $600 by 1980.

- Sovereign restructuring deals led to renewed doubts over currency stability.

- Investor appetite for gold surged as local bond yields collapsed.

2008 Global Financial Crisis

The collapse of Lehman Brothers and the ensuing credit freeze triggered unprecedented central bank interventions. Key observations include:

- Gold climbed from roughly $700 in early 2008 to above $1,000 by mid-2009.

- Massive quantitative easing programs raised concerns over long-term currency debasement.

- Safe-haven flows into gold ETFs drove record inflows, underlining its role as a liquidity and safe haven instrument.

Eurozone Sovereign Debt Turmoil

Greece’s debt crisis and Ireland’s bank bailouts in the early 2010s exemplified regional spillovers. Market reactions included:

- Euro depreciation against the dollar, making gold cheaper for non-euro investors.

- Gold surging past $1,900 per ounce in 2011 as fears of sovereign default peaked.

- Central banks in emerging markets increasing reserves to diversify risks.

Future Outlook and Strategic Implications

Looking ahead, several trends will likely shape the correlation between world gold price and global debt trajectories.

Rising Debt-to-GDP Ratios Worldwide

By 2025, many advanced and developing economies are projected to exceed 100% debt-to-GDP levels. This pressure could:

- Maintain robust gold demand as a hedge against potential currency crises.

- Fuel further central bank purchases, boosting official sector reserves.

Monetary Policy Divergence

With some central banks tightening and others easing, cross-border capital flows may favor gold as a non-yielding asset. Investors will watch real interest rates closely—when negative, gold’s opportunity cost falls, enhancing its allure for investment portfolios.

Technological and Regulatory Shifts

Innovation in digital gold trading platforms and exchange-traded products could broaden market access. Meanwhile, stricter regulation of commodity derivatives may dampen speculative excesses, potentially leading to:

- Reduced volatility through improved transparency.

- Greater institutional participation, supporting price stability over longer horizons.

Portfolio Diversification Strategies

Institutional and retail investors alike are recalibrating their asset mixes. Gold’s low correlation with equities and bonds makes it an effective diversifier, particularly when debt sustainability questions intensify. A balanced portfolio might allocate 5–15% to gold, depending on risk tolerance and macro outlook.