The trajectory of the gold market over the past century has been shaped by geopolitical shifts, economic policies and evolving investor behavior. Examining how gold prices responded to each era’s distinctive circumstances provides insights into broader trends in finance and risk management. From fixed exchange rate regimes to the rise of digital trading platforms, the precious metal has remained a cornerstone of portfolio diversification and a barometer of global economic sentiment.

Fixed Rates and Early Volatility

Under the Bretton Woods system (1944–1971), most world currencies were pegged to the U.S. dollar, itself convertible into gold at $35 per ounce. This arrangement created an artificial stability but concealed underlying imbalances in trade and fiscal policies. Several key episodes punctuated this era:

- Suez Crisis (1956): Political turmoil in the Middle East triggered concerns over oil supplies, leading to a modest defiance in the gold price as investors sought a safe haven.

- U.S. Balance of Payments Deficit: Persistent U.S. deficits eroded confidence in the dollar’s gold convertibility. Central banks began redeeming dollars for gold, piling pressure on reserves.

- London Gold Pool (1961–1968): Eight central banks collaborated to maintain the $35 peg by selling gold into the market. Despite coordinated efforts, speculative demand mounted, and the system strained under growing arbitrage.

Breakdown of Bretton Woods

President Nixon’s “temporary” suspension of gold convertibility in August 1971 marked a watershed moment. As fiat currencies replaced fixed standards, gold prices began a soaring path fueled by new market liberalization and floating exchange rates.

Floating Rates and Price Explosion

With the collapse of fixed rates, gold transformed from a monetary anchor to a speculative and protective asset. Key factors driving the newfound volatility included:

- Inflation Surge of the 1970s: Loose fiscal policies, oil shocks of 1973 and 1979, and wage-price spirals triggered double-digit inflation. Investors flocked to gold as a hedge.

- Geopolitical Risk: The Iranian Revolution and Afghan invasion by the Soviet Union heightened safe-haven demand.

- Central Banks: Some national banks began diversifying reserves, gradually selling gold in previous decades but adding back exposure as prices rose.

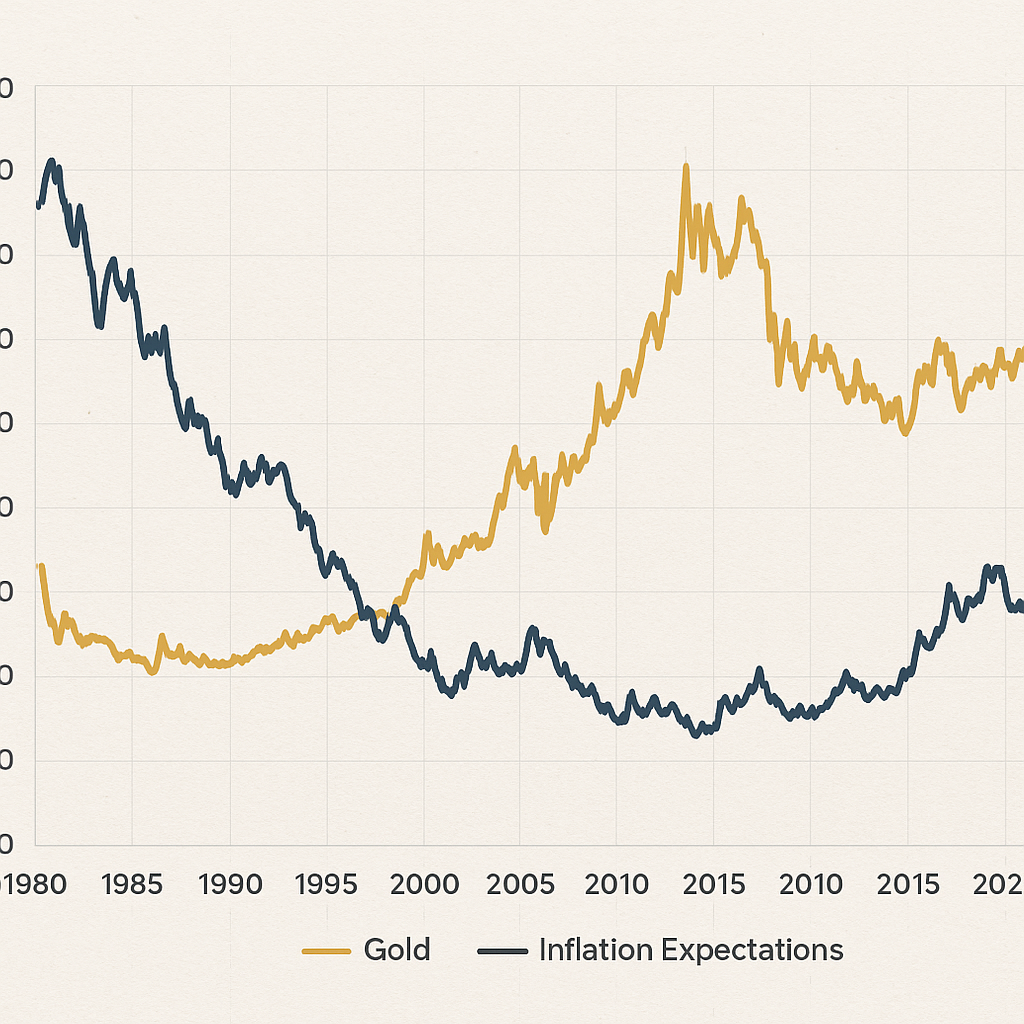

Between 1971 and 1980, gold prices surged from $35 to over $800 per ounce, representing a nearly twenty-fold increase in nominal terms. Volatility peaked in 1980 when speculative fervor collided with expectations of runaway inflation.

1980 Peak and Mean Reversion

After hitting all-time highs around $850, a combination of rising real interest rates, aggressive monetary tightening by the U.S. Federal Reserve and a slowdown in inflation pressured gold downward. Through the 1980s and much of the 1990s, prices trended in the $300–$400 range, reflecting diminished risk appetites and competing assets like equities offering higher yields.

Modern Era: Central Banks and ETF Revolution

Following two decades of subdued prices, the 21st century ushered in renewed interest in gold, prompted by systemic crises and evolving market infrastructure.

2008 Financial Crisis

The collapse of Lehman Brothers and near-failure of major banks exposed global financial fragility. Central banks slashed interest rates to near zero and launched quantitative easing programs, igniting concerns over currency debasement. Gold prices responded strongly, climbing from around $650 (2008) to over $1,900 by 2011.

Introduction of Gold ETFs

In 2003, the first gold-backed Exchange-Traded Fund (ETF) debuted. By tokenizing physical gold into shares, the vehicle democratized access, allowing retail and institutional participants to trade gold as easily as equities. Key impacts included:

- Enhanced liquidity and price discovery.

- Broader demand from pension funds, endowments and retail accounts.

- A transparent link between ETF holdings and global supply of gold bars in secure vaults.

By the mid-2010s, ETFs held over 2,000 tonnes of gold, cementing their role in price-setting mechanisms.

Regional Demand and Supply Dynamics

While Western markets advanced in financial engineering, emerging economies fueled physical demand. India and China, with deep cultural and industrial ties to gold, accounted for nearly half of annual global consumption.

- Rural and urban Indian markets: Weddings and festivals sustain year-round purchases.

- Chinese industrial use: Electronics, medical devices and renewable energy sectors boosted fabrication.

- Middle Eastern reserves: Petrodollar recycling led sovereign wealth funds to diversify through gold.

Technological Shifts and Future Outlook

The rise of digital trading platforms, algorithmic strategies and blockchain-based tokenization hint at new frontiers for gold markets. Key trends include:

- Tokenized Gold: Fractional ownership through blockchain reduces entry barriers and enhances settlement speed.

- Central Bank Digital Currencies (CBDCs): Potential to blur lines between sovereign money and alternative stores of value.

- Environmental, Social and Governance (ESG) criteria: Pressure on mining companies to adopt sustainable practices.

- Hedging Innovations: Options, futures and structured products continue to evolve, providing sophisticated tools to manage volatility.

As global growth cycles ebb and flow, gold remains a sentinel asset reflecting shifts in monetary policy, geopolitical tension and technological progress. Whether serving as a crisis protector, inflation hedge or portfolio diversifier, its centuries-old appeal endures in an ever-changing financial landscape.