Central bank decisions shape the trajectory of global financial markets, with **gold** often standing at the forefront of investor attention. As policymakers adjust tools to combat **inflation** or spur growth, the ripple effects on **gold** prices can be profound. This article explores how the actions of **central banks**, particularly changes in **interest rates**, **liquidity** injections, and unconventional easing measures, influence the demand for **gold** and how market participants adjust their **asset allocation** to include this **safe-haven** commodity amid rising **volatility**.

The Role of Central Bank Policies in the Gold Market

Monetary Strategies and Market Sentiment

When a major central bank signals a shift in its **monetary policy**, traders instantly reassess the relative attractiveness of **gold** versus interest-bearing assets. A decision to hold rates steady may reinforce the status quo, but hints of future cuts can drive investors toward **gold**, anticipating lower yields elsewhere. Conversely, hawkish rhetoric and rate-hike projections can dampen **gold**’s appeal, since higher borrowing costs strengthen currencies like the US dollar, making non-yielding **gold** relatively more expensive for foreign buyers.

Market sentiment can pivot rapidly on central bank minutes, speeches, or economic projections. Unexpected announcements by the Federal Reserve or the European Central Bank often trigger sharp moves in **gold** prices. These fluctuations highlight how sensitive **gold** is to changes in investor expectations around policy tightening or easing. Traders watch the Fed’s dot plot, the ECB’s inflation forecasts, and inflation swaps to predict the likely path of rates—and adjust their **gold** positions accordingly.

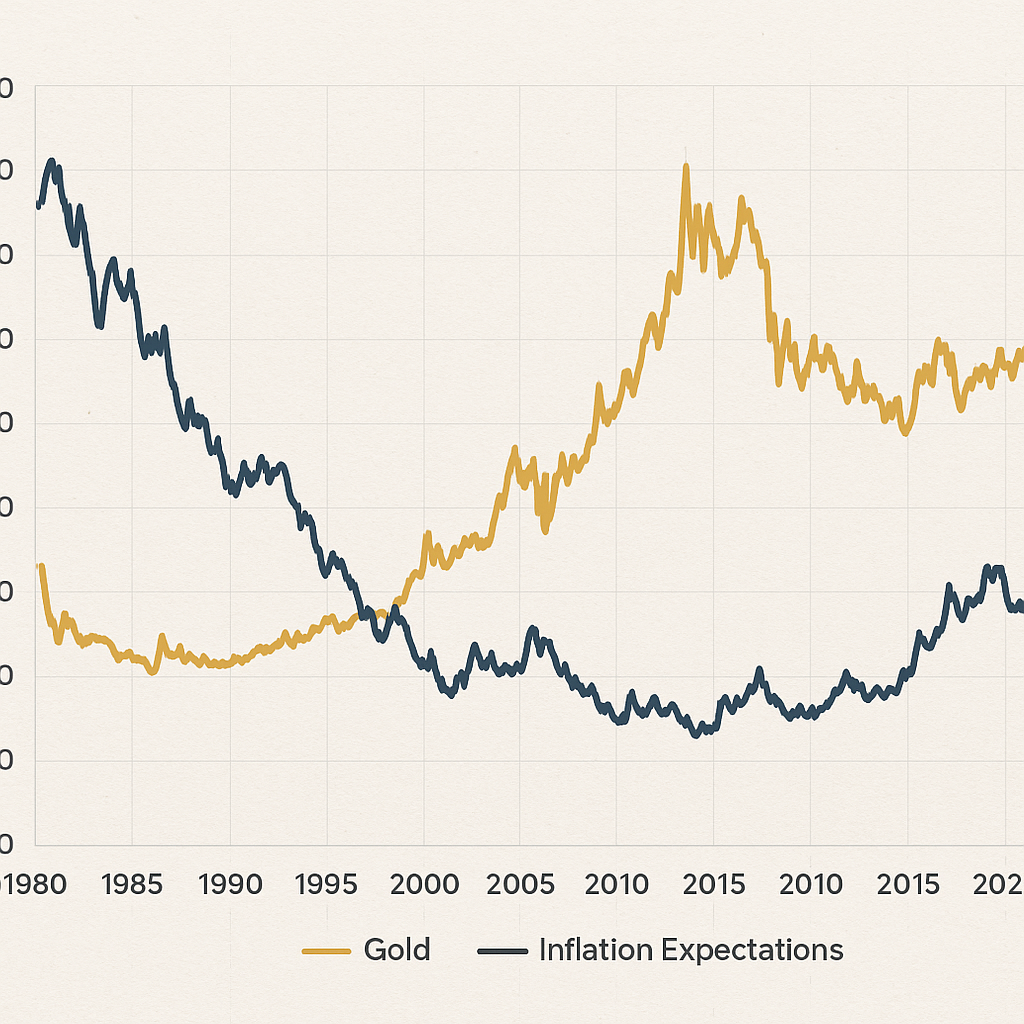

Inflation Control and Gold Demand

Since **gold** is commonly perceived as an inflation hedge, elevated consumer price pressures often boost its demand. Central banks tighten policy by raising **interest rates** to curb **inflation**, but there is often a lag before these measures fully take effect. During that interval, investors may increase **gold** holdings to protect purchasing power. Prolonged high inflation accompanied by policy uncertainty tends to catalyze substantial inflows into gold ETFs and physical bullion markets.

In emerging markets, central banks sometimes face the dual challenge of containing **inflation** while supporting growth. When they deploy aggressive rate hikes, local currencies may strengthen, slightly reducing domestic **gold** prices. Yet persistent inflationary pressures can sustain robust consumer demand for **gold jewelry** and sovereign reserves, underscoring the nuanced interplay between policy actions and market behavior.

Interest Rates, Liquidity, and Gold Prices

Rate Hikes vs. Rate Cuts

Higher **interest rates** increase the opportunity cost of holding **gold**, which does not yield coupons or dividends. Every basis point hike can translate into diminished allure for **gold** in contrast to bonds or savings accounts. On the flip side, when central banks embark on rate cuts to stimulate economic activity, they often expand their balance sheets, inject fresh **liquidity**, and weaken the currency. This environment typically favors **gold**, boosting its status as a hedge against currency debasement.

Liquidity Operations and Market Depth

Through open market operations and **quantitative easing**, central banks flood the financial system with cash. Enhanced **liquidity** can fuel speculative flows into **gold**, driving prices higher irrespective of underlying fundamentals. However, should liquidity measures be withdrawn abruptly—a process known as tapering—liquid markets may witness swift retracements in **gold** valuations as margin calls and redemptions cascade through leveraged positions.

- Excess **liquidity** often correlates with higher **gold** prices.

- Tapering of asset purchases can trigger short-term price corrections.

- Central bank swap lines influence global dollar funding conditions and indirectly affect **gold**.

Quantitative Easing, Tapering, and Their Effects

Unconventional Monetary Tools

In the aftermath of crises, central banks resort to **quantitative easing** (QE) to lower long-term yields and encourage spending. QE amplifies balance sheets and signals ongoing accommodation. For **gold**, this environment can be highly supportive; an expanding central bank balance sheet is often interpreted as future currency dilution. As a result, investors increase **gold** allocations as a store of value and a shield against potential inflation spikes.

Policy Normalization and Gold Corrections

As economic recovery gains traction, central banks may contemplate policy normalization—raising rates and reducing asset holdings. This process can create headwinds for **gold**, as improved growth prospects shift the risk-reward calculus back toward equities and bonds. Yet if policymakers misjudge the pace of tightening, triggering financial stress, **gold** may reclaim its role as a **safe-haven** asset, rallying on fears of a downturn or renewed market turbulence.

Geopolitical Risks, Safe-Haven Demand and Future Trends

Interplay Between Policy and Global Unrest

Geopolitical tensions—trade disputes, conflicts, or sanctions—often coincide with aggressive central bank interventions. In such scenarios, **gold** benefits from dual tailwinds: fear-driven safe-haven buying and loose monetary conditions intended to stabilize economies. Investors monitor central bank statements closely during crises, as coordinated easing can amplify **gold** rallies even further.

Long-Term Asset Allocation Shifts

Institutional investors increasingly view **gold** as a strategic diversifier within multisector portfolios. As central banks navigate the trade-offs between growth and **inflation**, asset allocators may tilt toward **gold** to enhance resilience against policy missteps. Emerging trends, such as central bank purchases of physical bullion for foreign reserve diversification, underscore a broader recognition of **gold**’s enduring value in a world of uncertain policy trajectories.

Future **gold** price dynamics will hinge on the evolving stance of major central banks, the trajectory of **interest rates**, and the global economic outlook. While no single factor guarantees a sustained uptrend or decline, the interplay between monetary policy and geopolitical developments will remain a key driver of **gold** market behavior for years to come.