The allure of gold has transcended centuries, cementing its position as a cornerstone of wealth preservation and financial security. From ancient civilizations to modern portfolios, this precious metal continues to captivate investors and governments alike. The global market for gold is a dynamic arena influenced by a multitude of factors ranging from geopolitical tensions to evolving monetary policy decisions. As central banks deepen their reserves and retail demand fluctuates, a critical question emerges: will gold ever lose its shine?

Historical Performance and Its Implications

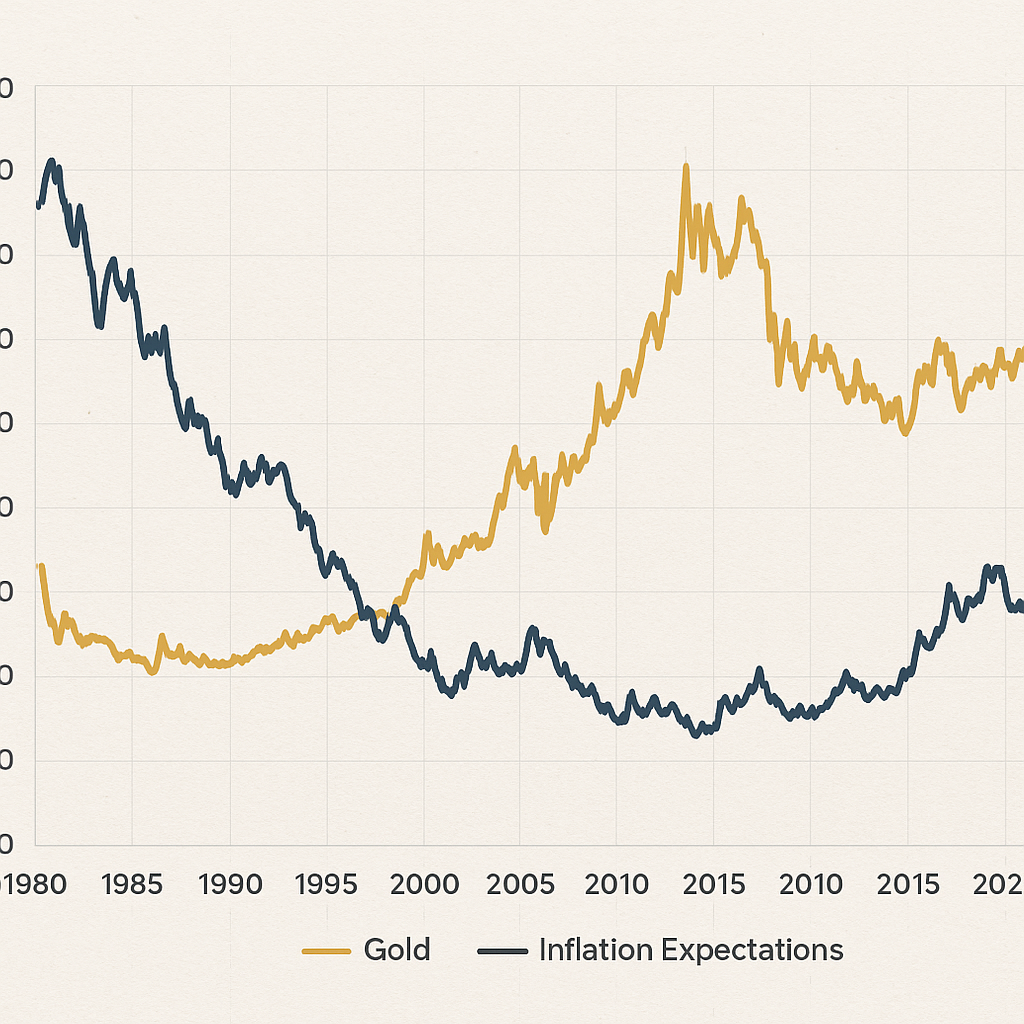

Gold’s trajectory over millennia highlights its enduring status as a reliable store of value. During the Roman Empire, gold coins underpinned vast trade networks, while in the 19th century, the Gold Standard anchored international currencies to fixed weights of metal. Even after the abandonment of the standard in 1971, prices skyrocketed, reflecting gold’s unique appeal as a hedge against economic uncertainty.

Between 2000 and 2011, gold saw an unprecedented bull run, surging from roughly $300 per ounce to over $1,900. This explosion was fueled by concerns over global debt, expanding money supply, and a weakening dollar. Despite occasional corrections, gold has historically rallied at critical inflection points, including the 2008 financial crisis and periods of soaring inflation.

Lessons from Past Cycles

- Safe haven demand rises during market stress.

- Central banks shift allocations, buying more in times of uncertainty.

- Supply disruptions—whether from mining constraints or geopolitical events—tighten markets.

- Investor sentiment can drive speculative rallies beyond fundamental value.

The historical performance of gold underscores its resilience, yet also reveals cycles of volatility. After a peak in 2011, prices corrected for several years before finding renewed momentum in 2019. These patterns suggest that while gold remains robust, it is not immune to extended periods of consolidation.

Key Drivers of Gold Price Fluctuations

Understanding the forces that propel gold prices is essential for anticipating future trends. Four primary categories shape the global gold landscape:

Monetary Trends and Central Bank Policies

Central banks around the world hold gold as part of their foreign reserves. In recent years, institutions from Russia to China have ramped up purchases, viewing gold as a counterbalance to currency risks. Policy decisions by the Federal Reserve, European Central Bank, and others impact real interest rates, which inversely correlate with gold’s opportunity cost.

Inflationary Pressures and Economic Indicators

Gold often thrives under high inflation environments. As consumer prices rise, fiat currencies lose purchasing power, making tangible assets more attractive. Key metrics such as the Consumer Price Index (CPI) and Producer Price Index (PPI) are closely monitored by market participants seeking to gauge future price directions.

Geopolitical Uncertainty and Market Sentiment

Gold’s status as a “safe haven” becomes pronounced during geopolitical crises. Wars, diplomatic standoffs, and trade disputes drive investors toward precious metals. Sentiment indicators, including the Commitment of Traders (COT) report and funding rates in gold futures, provide insight into speculative positioning and potential inflection points.

Supply-Demand Dynamics

Global gold supply consists of mine production, recycling, and central bank sales. Demand segments include jewelry, technology, and investment bars and coins. Emerging markets, particularly India and China, account for a significant share of jewelry consumption. Meanwhile, investment demand can surge in response to financial instability or currency devaluation.

- Mining output faces long lead times and environmental constraints.

- Recycling volumes respond to price incentives for scrap gold.

- ETF flows reflect institutional hedging behavior and strategic asset allocation.

The Future Outlook: Will Gold Ever Lose Its Shine?

While no asset is impervious to fluctuations, gold’s unique characteristics bolster its enduring appeal. Several factors suggest that gold will maintain relevance in global portfolios:

- Persistent global debt levels keep real yields near historic lows, supporting gold’s attraction as a non-yielding asset.

- Ongoing central bank diversification away from dominant reserve currencies.

- Technological advancements in gold extraction and refined processing reduce some supply bottlenecks, but cannot eliminate scarcity.

- Rising retail adoption through digital platforms and gold-backed cryptocurrencies enhances accessibility.

Nevertheless, challenges remain. A sustained rally in bond yields or a sudden surge in the US dollar could pressure gold prices. Additionally, breakthroughs in alternative assets—such as widely accepted stablecoins or tokenized commodities—may introduce new competition.

In weighing these scenarios, investors should consider gold not in isolation but as part of a diversified approach to risk management. Its performance relative to equities, bonds, and emerging asset classes will shape its role in future portfolios. Even as market structures evolve, the fundamental drivers of supply-demand imbalance, geopolitical risk, and inflationary hedging persist, suggesting that gold’s shine is far from dimming in the foreseeable horizon.