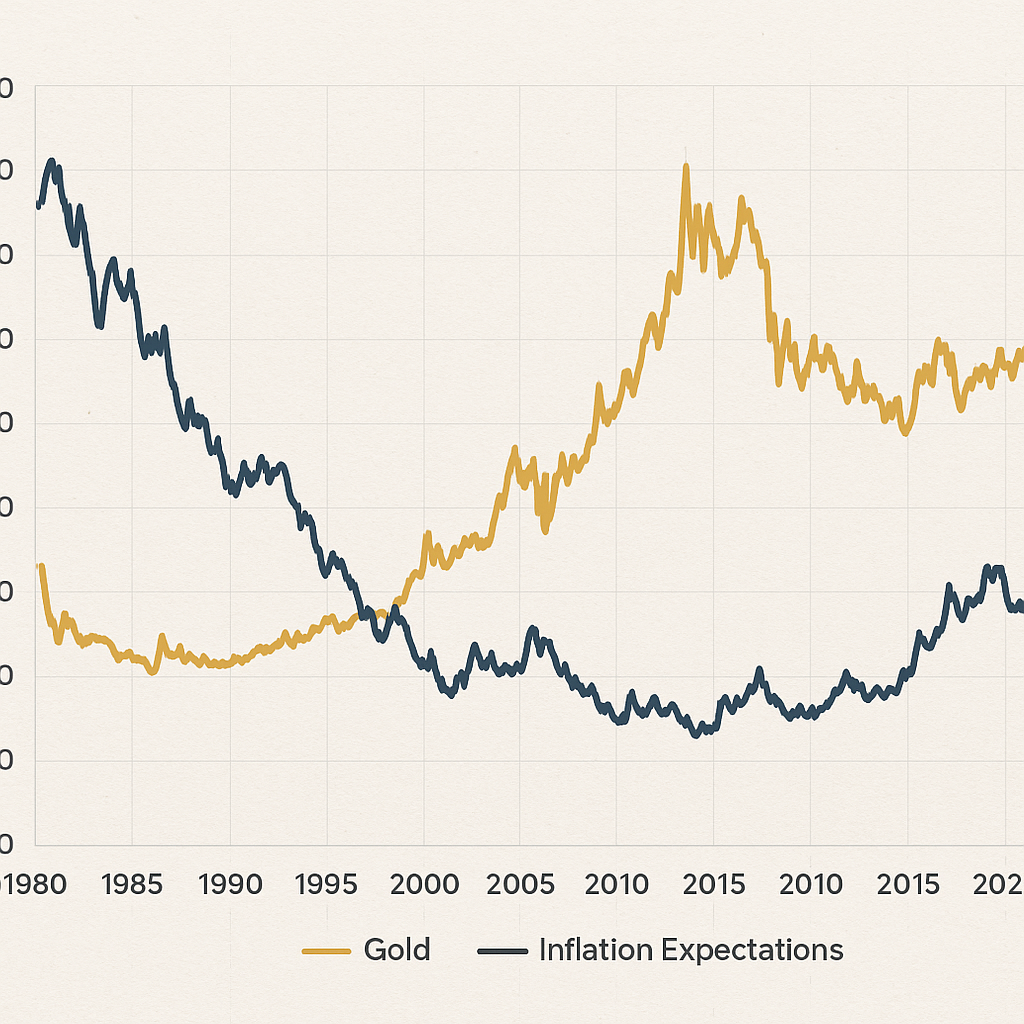

The relationship between armed conflict and the gold market has been a persistent theme throughout modern history. Wars force governments to seek financing, disrupt trade routes, and challenge existing monetary systems, creating ripples that often raise gold’s perceived value. From the trenches of World War I to contemporary geopolitical tensions, each conflict reshapes supply-demand dynamics and influences the global currency landscape.

World War I and the Rise of Gold as a Monetary Anchor

Prior to 1914, many major economies adhered to the classical gold standard, under which paper money could be freely exchanged for a fixed quantity of gold. This system promoted price stability and free trade. However, when war broke out, countries quickly suspended gold convertibility to finance massive military expenditures. Governments issued fiat currency without the backing of physical gold, leading to runaway inflation and currency devaluations.

- Suspension of convertibility: Britain, Germany, France, and other belligerents halted gold payments almost immediately to print war bonds and pay soldiers.

- Post-war reparations: The Treaty of Versailles imposed heavy reparations on Germany, paid partly in gold, straining its reserves and destabilizing the European financial system.

- Market confidence: Uncertainty about government solvency led traders to regard gold as the ultimate safe-haven, driving speculative hoarding and a surge in physical demand.

When hostilities ceased in 1918, nations faced staggering debts and inflationary pressures. Attempts to return to the gold standard in the 1920s proved difficult: exchange rates were realigned at different parity levels, creating misaligned currencies and deflationary pressures in some economies, particularly Britain.

World War II and the Bretton Woods System

As tensions rose again in the 1930s, many countries abandoned the gold standard altogether, preferring managed exchange rates. World War II further depleted European and Asian gold reserves, while the United States emerged with the bulk of the world’s bullion. In 1944, delegates at Bretton Woods designed a new monetary order that placed the U.S. dollar at the center, pegging it to gold at $35 per ounce.

- IMF and World Bank creation: These institutions aimed to stabilize currencies, encourage reconstruction, and prevent competitive devaluations.

- Fixed exchange rates: Countries maintained narrow currency bands relative to the dollar, with the right to draw on the IMF in case of balance-of-payments crises.

- U.S. gold reserves: At war’s end, the U.S. held over 20,000 metric tons of gold, cementing its role as a global financial anchor.

During this era, gold’s official price remained static, but private demand fluctuated. Many citizens viewed gold coins and jewelry as protection against inflation and political turmoil, while black-market trading emerged in countries with strict capital controls.

The Cold War, Decolonization, and the Breakdown of Fixed Rates

The postwar peace was marred by the Cold War’s ideological standoff, proxy wars, and the process of decolonization. Each new conflict—from the Korean War to the Algerian struggle—required large-scale military spending, contributing to government deficits and rising inflation in the 1950s and 1960s. Meanwhile, newly independent nations began to claim portions of colonial gold stocks and establish national gold reserves, diversifying their foreign assets.

Vietnam War and Fiscal Pressures

The Vietnam conflict prompted substantial American military outlays, financed by Treasury debt rather than increased taxes. By the late 1960s, mounting U.S. deficits triggered doubts about the dollar’s convertibility into gold, as nations like France started demanding physical bullion in exchange for dollars held in their central banks.

Nixon Shock and End of Bretton Woods

In August 1971, President Nixon closed the “gold window,” halting the exchange of dollars for gold. This move ended the Bretton Woods system and ushered in an era of floating exchange rates. Gold prices were liberated from their fixed $35 peg and soared. Between 1971 and 1980, the official price skyrocketed, fueled by market volatility, geopolitical crises (such as the 1973 oil embargo), and rampant inflation.

Modern Conflicts and Contemporary Gold Dynamics

As the Cold War wound down, the gold market settled into new patterns. However, subsequent interventions—such as the Gulf War in 1990–1991, the U.S.-led campaigns in Afghanistan and Iraq, and tensions in Eastern Europe—continued to influence investor psychology and central bank policies.

- Safe-haven demand: In times of crisis, from 9/11 to the 2008 financial meltdown, gold’s allure as a protective asset intensified.

- Central banks accumulation: Emerging economies like China, India, and Russia have steadily increased purchases, diversifying away from the U.S. dollar and reinforcing gold’s role as a strategic reserve asset.

- Quantitative easing: Post-2008, major central banks flooded markets with liquidity. Concerns over debasement of fiat money amplified interest in physical gold and gold-backed ETFs.

- Supply chain challenges: Mining disruptions in conflict regions (e.g., West Africa, South America) occasionally constrain supply, nudging prices upward.

The 21st-century gold market is thus a tapestry woven from lessons of the past: ongoing skirmishes, shifting alliances, and monetary policy pivot points. Gold no longer underpins currency but acts as a hedge against uncertainty and a barometer of global geopolitics. Investors often adjust positions based on expectations of rising inflation or fresh crises that spur risk aversion flows into bullion.

Future Outlook: Emerging Threats and Gold’s Enduring Role

Looking ahead, potential flashpoints—from cyber warfare to territorial disputes in the South China Sea—could once again tilt the scales toward precious metals. As digital currencies and instant settlement platforms evolve, gold’s tangibility and historical track record offer a counterbalance to purely virtual assets. Central banks remain wary of overexposure to any single currency, ensuring that gold continues to occupy a vital place on their balance sheets.

In an interconnected world, armed conflicts still ripple through financial markets. Gold’s journey through two world wars, a Cold War, and multiple regional wars underscores its status as both a mirror of global strife and a bulwark of monetary confidence. Its price will rise and fall, but its symbolic and practical importance endures, reminding us that even amid modern innovations, age-old metals can carry profound economic weight.