The enduring relationship between gold and inflation expectations has intrigued economists and investors for decades. While central banks adjust monetary policy to stabilize prices, precious metals markets continually react to changes in future price outlooks. This article explores how the long-term correlation between gold prices and inflation expectations has evolved, the mechanisms underlying this link, empirical findings from major studies, and the implications for investors and policymakers seeking to balance risk and return in diverse economic environments.

Historical Evolution of Gold and Inflation Expectations

Gold as a Baseline Monetary Standard

Under the classical gold standard of the 19th and early 20th centuries, the price of gold remained relatively fixed against major currencies. Price levels fluctuated within narrow bands, and confidence in money’s purchasing power anchored inflation at low levels. The breakdown of the gold standard during World War I and again in the 1930s liberated governments to pursue expansionary policies, which led to higher and more variable inflation. During these periods, gold transitioned from official backing to an alternative store of value, prompting a reassessment of its relationship to inflationary pressures.

Post–Bretton Woods and Rising Price Uncertainty

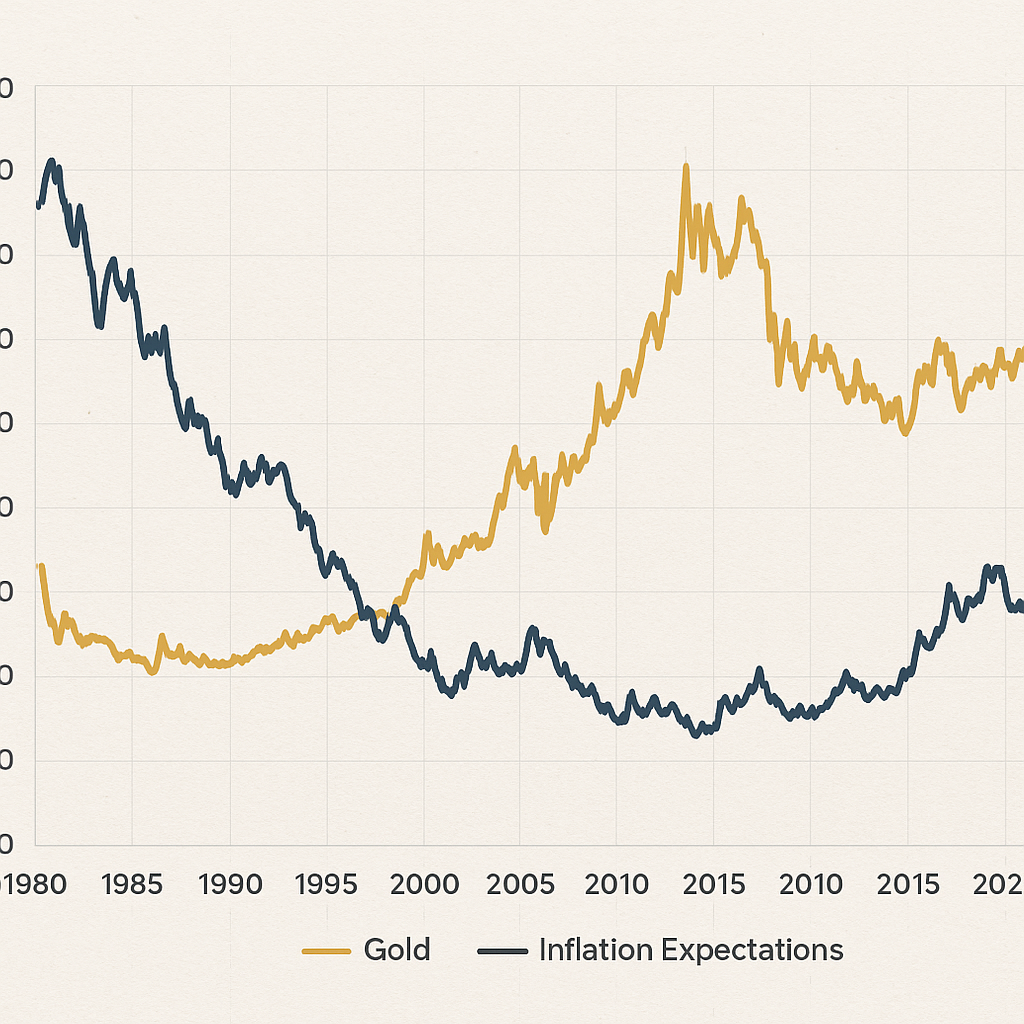

The collapse of the Bretton Woods system in 1971 marked a decisive shift. Currencies floated freely and oil shocks amplified price shocks. Inflation expectations soared, as did the market value of gold, which surged from around $35 per ounce to over $800 by 1980. This era crystallized gold’s reputation as a hedge against elevated inflation, but also revealed its volatility. Sharp swings in consumer price indices and uncertain monetary forecasts turned gold into a barometer of future pricing trends.

Mechanisms Linking Gold and Inflation Expectations

Opportunity Cost and Real Yields

Gold offers no coupon or dividend, so its attractiveness depends on alternative real returns. When real interest rates (nominal rates minus expected inflation) decline, holding gold becomes relatively more appealing. A drop in real yields erodes the opportunity cost of owning bullion. Conversely, rising real returns on bonds can dampen demand for gold as investors shift toward income-generating assets.

Flight to Safety and Risk Aversion

In times of geopolitical stress or financial turmoil, gold often draws capital seeking a safe haven. Heightened risk aversion coexists with surging inflation expectations, as concerns about currency debasement and policy missteps drive investors toward tangible assets. Central bank interventions, currency devaluations, and banking crises amplify this dynamic, reinforcing the strong linkage between price outlooks and precious metals demand.

Market Sentiment and Behavioral Drivers

Investor psychology plays a crucial role. Surveys of market participants, positions in futures markets, and flows into exchange-traded funds collectively signal evolving expectations. Social media chatter, economic forecasts, and macroeconomic data releases shape sentiment. Bullish gold sentiment often coincides with rising break-even inflation rates derived from Treasury Inflation-Protected Securities (TIPS), indicating a close alignment between qualitative attitudes and quantitative measures.

- Shifts in central bank communications and guidance

- Movements in commodity and energy prices

- Global growth outlooks and currency fluctuations

- Technical trading patterns and speculative positioning

Empirical Studies and Data Analysis

Cross-Country Time-Series Evidence

Academic research over the past three decades has examined multi-country datasets to quantify the gold–inflation nexus. Many studies employ Vector Autoregression (VAR) models, Granger causality tests, and rolling correlation windows. Key findings reveal that the gold price responds positively to unexpected inflation surprises, particularly in advanced economies. Yet the strength of the relationship varies by regime: during low-inflation periods, the linkage weakens, while in high-inflation episodes, it becomes more pronounced.

Break-Even Inflation and Gold Returns

Another strand of research compares gold returns directly to break-even inflation rates implied by TIPS. Over the last two decades, rolling 10-year correlations between gold and the five-year break-even rate have averaged between 0.4 and 0.7, underscoring a moderate to strong long-term tie. However, in periods of monetary tightening or disinflationary shocks, this correlation can dip significantly or even turn negative for short intervals.

Volatility and Tail Events

Beyond average correlations, studies also focus on tail dependencies. Extreme inflation surprises—such as those experienced in the 1970s or during hyperinflation episodes—tend to coincide with outsized gold price jumps. This asymmetric behavior implies that gold offers some crisis insurance, albeit at the cost of heightened price swings under normal conditions.

Implications for Investors and Policymakers

Portfolio Construction and Diversification

Incorporating gold can enhance resilience against inflationary regimes. A modest allocation to bullion or gold-backed securities may reduce portfolio drawdowns when real rates fall and price pressures rise. However, the inclusion must be balanced against volatility and the lack of cash flow. Dynamic strategies, such as trend-following or momentum overlays, may further optimize timing and mitigate drawdowns in disinflationary periods.

Central Bank Reserves and Risk Management

Many central banks maintain gold reserves as part of their foreign exchange holdings. The historical track record suggests that bullion can help preserve purchasing power when fiat currencies weaken. Policymakers should monitor forward guidance and yield curve movements to anticipate potential shifts in gold demand and to manage the implied correlation risks within their reserve portfolios.

Alternative Inflation Hedges

While gold remains a widely recognized inflation hedge, investors also consider inflation-linked bonds, commodities baskets, real estate, and certain equities. Each instrument carries its own risk-return profile and sensitivity to macroeconomic surprises. A holistic approach compares expected payoffs under various inflation scenarios, balancing the cost of carrying non-yielding assets against the protection they offer against unexpected price shocks.